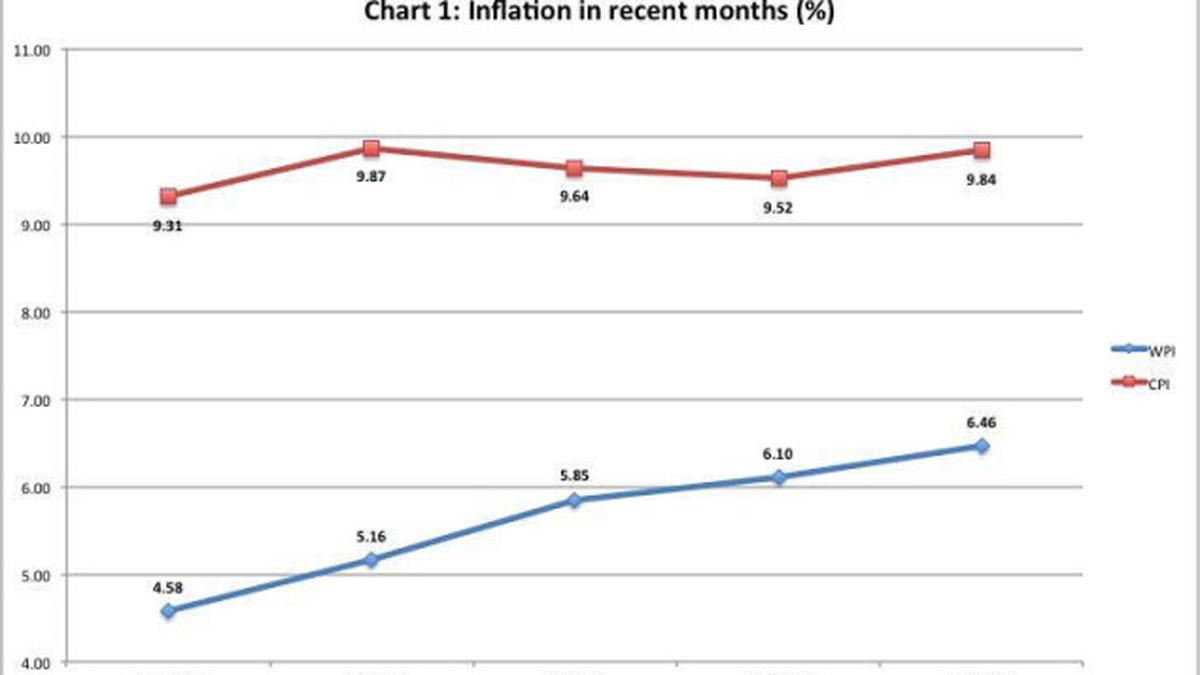

In his Second Quarter Review of Monetary Policy, Reserve Bank of India governor Raghuram Rajan was candid enough to admit that GDP growth in the country this year may be lower (at 5 per cent) than earlier expected, and that inflation remains a problem. The inflation rate as reflected by the Wholesale Price Index has risen and as measured by the Consumer Price Index remains uncomfortably high. India is experiencing stagflation, requiring the RBI to think of reining in inflation without damaging growth further and possibly reviving it a bit. That is a difficult call.

The centrepiece of the central bank’s policy response seems to be and was presented as a hike in the key interest rate, the repo rate, by 25 basis points from 7.5 to 7.75 per cent, to address inflation. However, that hike has been combined with a reduction in the marginal standing facility rate (from 9.0 to 8.75 per cent) and a measure to infuse additional liquidity into the banking system. The latter consists of increasing the liquidity provided through term repos of 7-day and 14-day tenor from 0.25 per cent of net demand and time liabilities (NDTL) of the banking system to 0.5 per cent with immediate effect.

Compare this with what the RBI governor did when he undertook the mid-quarter review of monetary policy this September. Then too he chose to hike the repo rate from 7.25 to 7.5 per cent arguing that the battle against inflation had not been won. On the other hand, he chose to lower the interest rate on the Reserve Bank of India’s marginal standing facility (MSF). Soon thereafter, in early October, the RBI strengthened its liquidity enhancement measures aimed at increasing bank access to lower cost funds by: (i) further reducing the MSF rate by 50 bps to 9 per cent; (ii) conducting open market operations (OMOs) involving the purchase of government securities to the tune of Rs. 9,974 crore to inject liquidity into the system; and (iii) providing “additional liquidity through term repos of 7- and 14-day tenors for a notified amount equivalent to 0.25 per cent of net demand and time liabilities (NDTL) of the banking system”. There are clearly signs of addiction to an unusual cocktail of policies involving an anti-inflationary hike in the key interest rate combined with increased access to cheaper liquidity.

What explains this choice of a combination of apparently conflicting measures? The repo rate is the rate at which banks borrow from the central bank against collateral that consists of excess holdings of securities that can serve to meet statutory liquidity ratio (SLR) targets. If banks are pushing credit, however, leading to a significant rise in the credit deposit ratio, then they are likely on occasion to need more liquidity than they can get by pledging/temporarily selling their “excess” SLR-type securities.

To increase bank access to ‘emergency’ liquidity so that they can keep pushing credit even if at slightly higher interest rates, the RBI had in 2011 established the marginal standing facility (MSF), under which banks can borrow against securities they hold as part of (and not just in excess of) their SLR requirements, subject to payment of a higher penal interest rate and with a ceiling to the amount of such borrowing they can resort to. The ceiling on resort to funds under this facility by banks was set at one per cent of their respective Net Demand and Time Liabilities outstanding at the end of second preceding fortnight.

Originally the MSF rate at which banks borrow had been set at 100 basis point or 1 percentage point higher than the repo rate. This differential was hiked to 2 percentage points in July 2013 in a move that seemed motivated by the need to curb speculation on the rupee. The September 2013 Mid-Quarter Review of Monetary Policy partially reversed that hike by reducing the differential between the MSF rate and repo rate to 1.5 percentage points. With the latest policy announcement, which increases the repo rate while reducing the MSF rate, the differential has come down to 1 percentage point. In addition, besides access to overnight funds under these facilities, the increase in the ceiling on term repos provides an additional and longer-term source of liquidity to the banks.

In sum, an important plank of monetary policy in recent times seems to be that of enhancing the ability of banks to push loans by increasing their access to emergency liquidity, the requirement for which may increase as a consequence of increased lending out of a given deposit base. The ‘penalty’ imposed for resorting to ‘excess’ borrowing from the central bank has also been reduced. So long as banks can find borrowers who are willing to pay the higher interest that lending backed by costlier (but cheapening) funding entails, they can lend more.

This is possibly expected to support growth, by permitting lending to the retail sector for financing purchases of automobiles, two-wheelers, durables and much else. The government on its part has agreed to facilitate this by infusing capital into the banking system, which would also enhance their lending power. In this way, the RBI expects to address inflation as well as back growth. While growth may be supported by credit-financed personal expenditures, it is unclear why the demand this generates would not add to inflationary pressures just because the repo rate is being hiked. Reading between the lines the argument seems to be that this would result in the higher repo rate “anchoring inflation expectations”, whatever that nebulous phrase may imply.