One more bi-monthly monetary policy review has come and gone, and the now not-so-new Reserve Bank of India Governor Raghuram Rajan and his team have chosen to sit tight. No change in the benchmark repo rate, no change in the CRR or SLR. This is the fourth consecutive policy review in which the repo rate has been left untouched at 8 per cent. This decision, not to lower interest rates as many sections have been demanding and not to infuse additional liquidity into the system, occurs at a time when growth is sluggish, but consumer price inflation on a point-to-point basis stood at a high 9.5 per cent in August. So the RBI’s decision is seen as reflecting an emphasis on combating inflation, even if that is at the expense of growth.

The repo rate, being the interest rate at which the central bank accommodates the short terms liquidity needs of the banking system, is an important influence on the structure of interest rates in India. High interest rates can adversely affect growth by discouraging industrial and agricultural investment as well as curbing the volume of debt financed household investment and consumption. This explains why interest rate reduction is expected when growth is sluggish. But the problem, the RBI argues, is that inflation is high. And reducing rates can aggravate inflation, which in its view can be worse for growth. Hence the stubborn insistence on holding interest rates steady.

This refusal to use the monetary policy lever to revive growth because of the fear of inflation is expressed in a context of fiscal conservatism. The government is committed to pruning expenditures in order to reduce the fiscal deficit and ensure fiscal consolidation. Since that implies a fiscal stance that does little to raise demand, the macroeconomic policy framework as a whole (or the combination of fiscal and monetary policies) is biased against spurring growth.

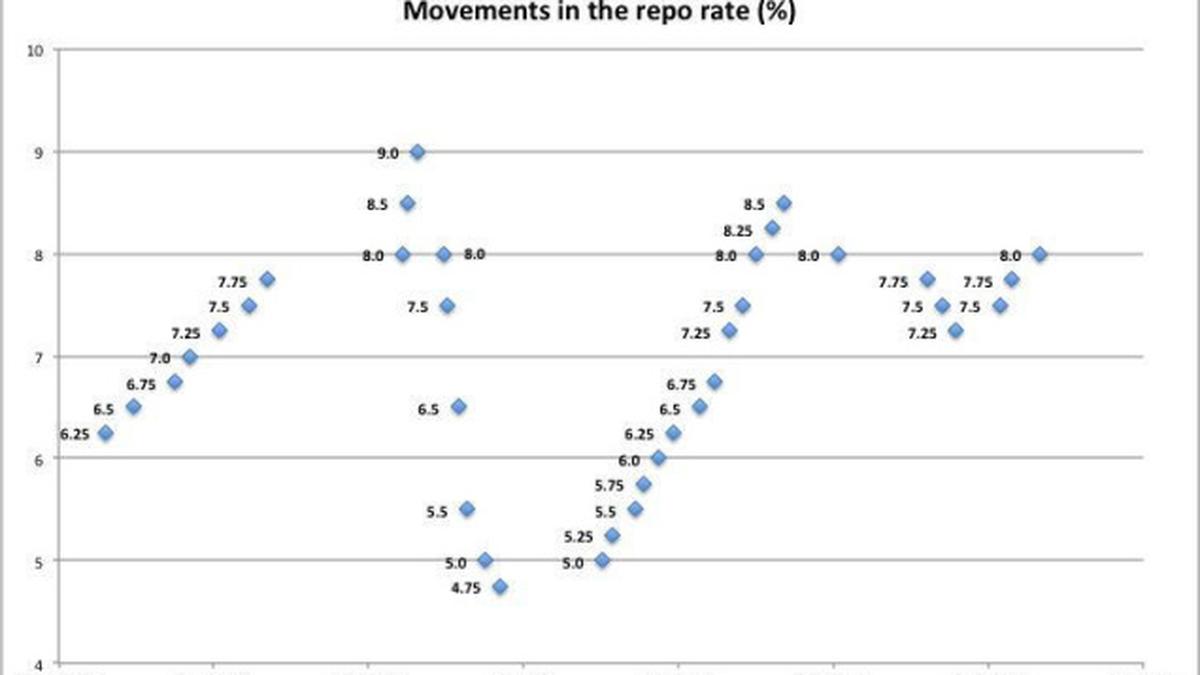

Unfortunately, this monetary policy stance is being adopted at a time when interest rates are high by recent historical standards. As the accompanying Chart shows, the repo rate has ruled at between 7 and 8.5 per cent for more than three years now, and the last time it was in this range was for about a year and half starting mid-2006. So what we are seeing here is not just a policy of holding nominal rates steady, but of sticking with a high nominal interest rate regime for a longish period. In fact, taking a longer view, other than for the 2009-10 period when the government was responding to the affects of the global crisis, the benchmark nominal interest rate has been relatively high for much of the last decade.

Interestingly, this has not helped rein in inflation, especially food price inflation, which has also been ruling high for a considerable period. All that the RBI can claim (but cannot prove) is that high interest rates have prevented inflation from being even higher. They have not helped bring down the rate of inflation. The RBI governor made a feeble effort to argue they have by pointing to “the steady decline in inflation excluding food and fuel by a cumulative 111 basis points since January 2014, to a new low.” The governor may find that significant, but those having to spend much of their incomes on food and fuel are bound to disagree. The fact that this failure on the inflation front combined with the pressure to do something for growth has not pushed the RBI to cut rates suggests that there could be factors other than inflation influencing the central bank’s interest rate policy.

One such influence can be the effect interest rates have on inflows of foreign portfolio investment. As noted earlier, the benchmark rate influences the structure of interest rates. And that structure in turn influences returns in financial markets. So a high interest rate regime is one way of encouraging foreign investments inflows and preventing outflows. That relationship seems to be confirmed by the large net inflows of foreign portfolio capital into India during the period of high interest rates. More recently, close to $14 billion has been invested in Indian equity markets since January this year, raising the Sensex by a lucrative 26 per cent. Moreover, a rising share of institutional investor inflows goes now into the debt rather than equity market (Refer “ >Bond Rush in Indian Markets ”, Business Line, September 2, 2014). Investors are clearly cashing in on the much higher interest rate in India than elsewhere and the impact that has on overall financial returns.

Reducing interest rates can have a damaging impact on these inflows and it is hard to believe that the RBI has not factored that into its decision on interest rates. If the RBI governor can express worry about the impact that the US taper and the consequent rise in US interest rates can have on investment flows to emerging markets like India, he is bound to be worried about the impact that lower interest rates in India can have on such flows. This then can be an important, even if not the sole, influence on the RBI’s monetary policy stance.

Many governments pursue fiscal consolidation to appease foreign financial interests that abhor deficits. A restrictive monetary policy with high interest rates also seems to be influenced by foreign finance. Clearly then, foreign finance is not good for growth, contrary to what the government seems to believe.