Till recently inflation was considered India’s No. 1 economic problem. That problem is no more the focus of attention, having been displaced by the widening current account deficit and the weakening rupee. This is not only because matters have worsened significantly on the external front. It is also because an impression has got around that the government or the central bank, or a combination of the two, have reined in inflation after a long effort. “Headline inflation”, it is argued, is now not as low as it should be but is by no means a major problem.

The question is what defines headline inflation? For long, point-to-point changes in the wholesale price index (WPI) were considered the headline inflation rate. The WPI is a weighted average of the prices of most goods produced in the economy, with the weights being their shares in domestic output and their prices those prevailing in wholesale markets. It is closer to a producer price index, reflecting more what producers charge their immediate buyers, rather than the prices that prevail at the end of the trading chain, in retail markets. Internationally consumer price indices rather than producer price indices are the standard for measuring inflation, since they reflect the prices that ordinary citizens face and pay. India does have multiple consumer price indices (for industrial workers, non-manual employees and agricultural/rural labourers) used to assess the increase in the prices paid by these sections for the commodity bundles they consume. However, inflation measured by the WPI was treated as the measure of headline inflation.

Early in 2012, the Central Statistical Organisation of the government of India released a new, national, monthly, consumer price index (CPI), with separate indices for rural and urban areas and covering a set of final consumption goods, weighted by their share in the consumption basket and with their prices collected from retail markets. The release was supposed to mark the transition to the use by the government and the central bank of this new index rather than the wholesale price index (WPI) to compute the headline inflation rate. Given that, it is surprising that barely a year and a half since annual point-to-point inflation rates have been calculated based on this index (which was first released for January 2011, making January 2012 the first month for which we have an annual rate), the government and the media have returned to focusing on WPI-based inflation.

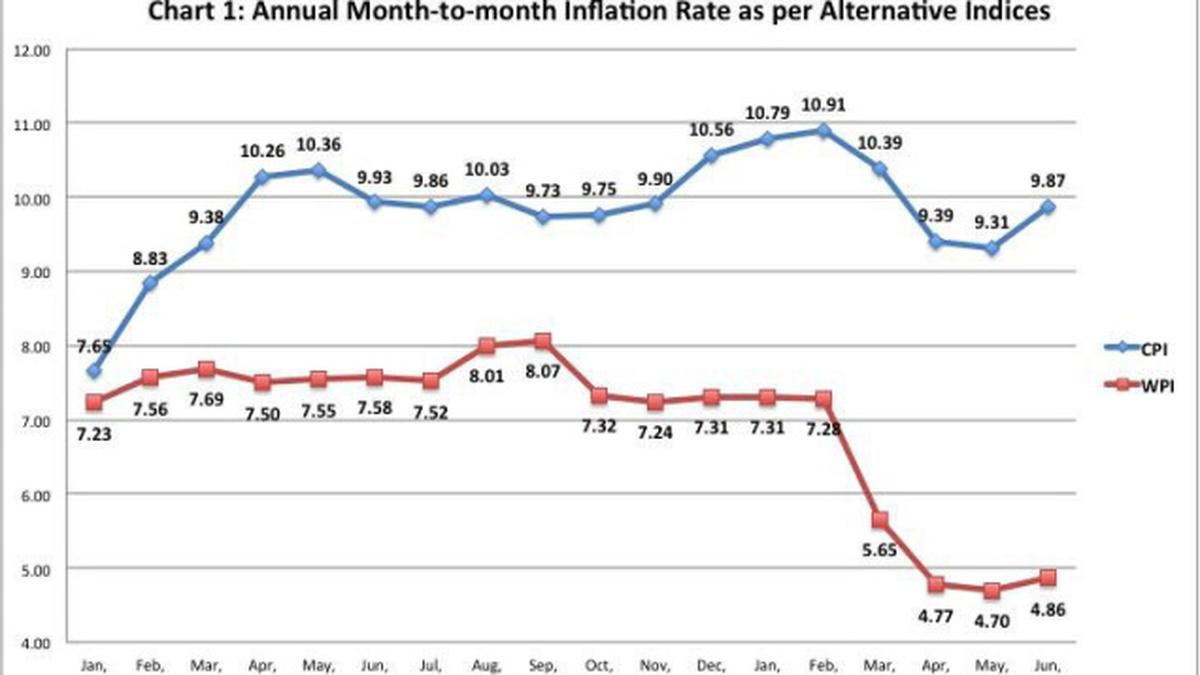

This does indeed make a difference. As >Chart 1> shows, trends in the month-on-month annual inflation rate differ substantially, depending on the index used to compute that rate. When measured using the WPI, inflation was running at 7-8 per cent between January 2012 and February 2013, and has since fallen to less than 5 per cent. However, when measured using the national CPI, it had risen from 7.7 per cent to 10.9 per cent between January 2012 and February 2013, and has since fluctuated between 9 and 10 per cent.

The reason for this significant difference partly lies in the substantial difference in rates of inflation across commodity groups as measured by the WPI. While Minerals, Fuel and Manufactures have registered significant declines in month-on-month inflation rates ( >Chart 2 ), and helped hold aggregate WPI-based inflation steady, inflation in Primary articles, especially non-Food primary articles, has remained high and even risen sharply during the early part of the period. Since many of these primary goods are likely to be consumed by the ordinary citizen and, therefore, feature in the CPI with a large weight, that index shows inflation to be much higher.

In the event, the government that had wanted to follow what it often terms “international best practice”, and shift to the CPI as an indicator of headline inflation, has chose to downplay the national CPI and the trends it reveals. While the CPI figures are routinely released, reference to inflation focus on the WPI, which is much less damaging as an indicator of inflation performance. Perhaps the difference between the government and the Reserve Bank of India on the level of inflation and therefore the need to persist with a high interest rate regime arises because the latter has one eye on inflation as measured by the not-so-new CPI. Being still high the RBI is for a tight money regime, which some in the government feel should be relaxed to spur growth, since inflation is down.

{kind=link}

{kind=link}