India’s aviation industry has been lobbying for a government bailout. With Kingfisher Airlines on the verge of bankruptcy, there are a number of ideas on how the bailout can be delivered: getting oil companies to lower aviation fuel prices, reducing taxes on fuel, persuading banks to restructure debt and offer new credit on easier terms, and changing the rules to allow foreign airlines to bring in capital in return for equity.

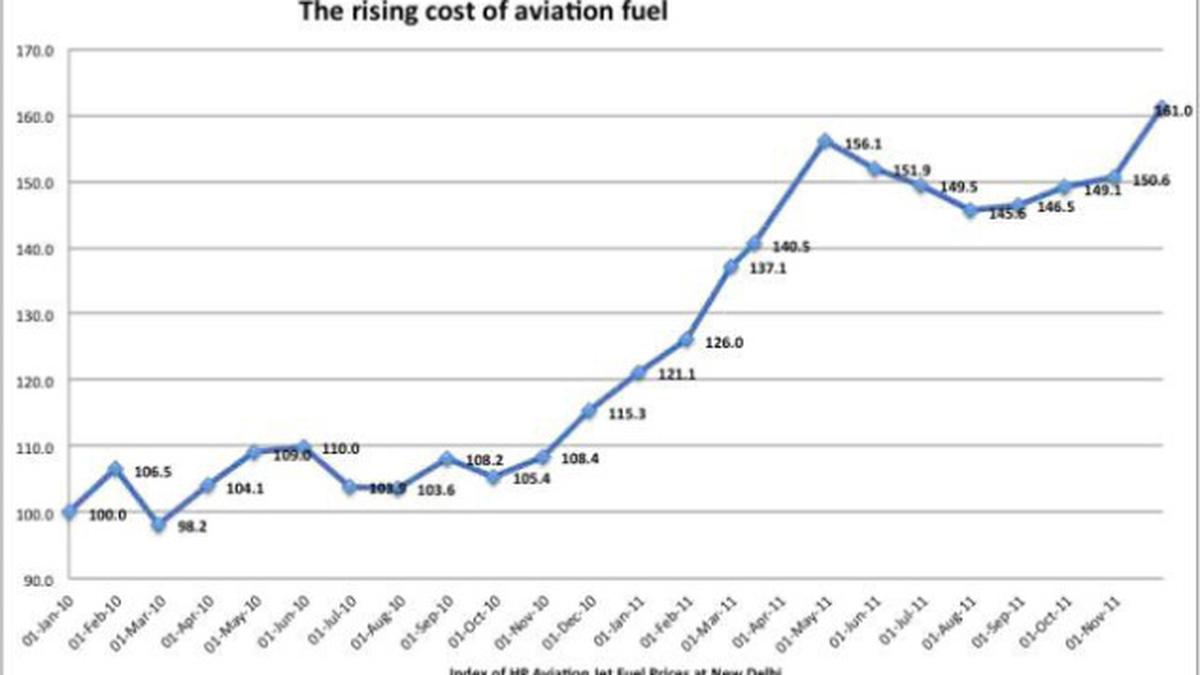

According to reports, promoters and top executives of leading private sector airlines met the Prime Minister late November to make their case. Their arguments went along expected lines: aviation fuel costs amount to as much as 40 per cent of operating costs; fuel prices have risen sharply; government taxes tend to push up prices even more; and aviation fuel prices in India are as much as 70 per cent higher than elsewhere in Asia. The net result according to them is a substantial loss that is challenging their viability. So the state must step in to rescue the airlines.

The sense is that the Prime Minister is inclined to intervene in their favour, though matters like FDI in retail have postponed the decision. Under other circumstances the PM’s stance may have appeared normal. The airline industry is an important part of the country’s infrastructure and the fuel price hike is an external shock threatening the survival of leading players. But fuel prices affect not only the airlines. Directly and indirectly they affect every segment of the population, including the poor and the middle classes. Yet the government in recent times has been clear that it will not go back on its decision to reduce fuel subsidies by doing away with the administered pricing mechanism and will stick with its policy of adjusting domestic prices when international prices change. Nor will it forego revenues by cutting duties on fuel any further. Money, the Prime Minister is reported to have said, does not grow on trees.

This difference in approach when it comes to preventing the erosion of the real incomes of ordinary citizens and to protecting the profits of the airlines is a striking anomaly. It is explained by the fact that part of the mess in aviation today is because of the government’s open skies policy. That policy was influenced by the view that opening up the airline industry to new and multiple private operators would enhance competition, reduce prices and improve the quality of customer service.

One danger, however, is that “competitive markets” often result in failure. Wrong decisions leading to excess capacities, price wars that reduce margins and just plain bad management can lead to losses and the bankruptcy of one or more players in the market. According to the votaries of the market mechanism this is inevitable. So when losses occur for these reasons, governments should not intervene but should let markets work. If some firms go bankrupt, so be it. It is merely the way in which the market imposes its discipline, penalising wrong decisions or poor management, and delivering a meaner, leaner and more efficient industrial landscape.

However, despite having opened up the airline sector on grounds such as these, the government has been reluctant to stick by these principles. In the Kingfisher case, it now transpires that the ailing airline has been on life support from three sources among others: huge volumes of credit from the banking sector, including public sector banks; a conversion of part of the loans provided by banks into equity such that the banks hold 23 per cent of the shares in the airline; and short term credit from the oil distribution companies on the aviation fuel being consumed by the airline. It has been known for some time now that the company had accumulated losses that exceeded its equity and reserves. But it was when the airline could not meet its bills for aviation fuel and the oil companies stopped supply on credit that the cancellations and the crisis began.

The story of how we got here is linked to the government’s liberalisation drive since the 1990s. The justification for that drive was that long years of monopoly ownership of the public sector in the airlines business had resulted in inefficiency and high costs and low profits or losses in Air India and Indian Airlines. Nobody would defend these public sector firms as being the paragons of efficiency. But the fact of the matter is that a whole host of “extraneous” factors affected the profits of Air India and Indian Airlines.

To start with, the functioning of these public sector entities was driven by objectives other than sheer profit. For example, they were required to fly on a number of unprofitable routes to ensure connectivity in a geographically large nation, including on routes to remote locations with relatively sparse traffic. Internationally, Air India was the nation’s carrier ensuring connectivity not just for commercial profit but for reasons related to diplomacy.

In sum, the profit criterion was for long subordinate to other objectives for the national carriers. This, however, did result in the misuse of the “freedom”, leading to unwarranted costs and losses that were ignored. To boot, with the ministry of civil aviation combining in itself the role of policy maker, investment decision maker and day-to-day monitor of the airlines operations, the companies were subject to excess intervention, were made the victims of wrong investment decisions and were forced to engage in activities that may not have been commercially or socially appropriate. Even now, for example, there is a controversy surrounding decisions with regard to aircraft purchases made before Air India and Indian Airlines were merged. Those acquisitions, which would require Air India to pay out huge sums when it has accumulated losses are seen as inappropriate in terms of route management and on financial grounds.

Given this evidence, what was required in the airline industry was an all out effort to revamp Indian Airlines and Air India. The revamp should have sought to ensure greater autonomy in functioning, institutional change to ensure transparency in investment and operational decision-making, and appropriate governance and monitoring mechanisms. Rather than focus on such changes, the government sought to induct private initiative into the airline industry on the grounds that the competition will improve overall efficiency.

As a result of that indiscriminate opening up, over the years the business has seen the entry of a large number of private players. Knowingly or unknowingly these investors had bought the argument that the only reason for the poor profit performance of the public sector airlines was their incompetence. Any number of efficient operators that could keep costs down and offer better services at a cheaper price would be able to quickly turn a profit. The net result was irrational investment, excess capacity on many routes and severe price competition on some. The government’s view was that this was merely a temporary process of adjustment. Wrong decisions by private operators would lead to a “shake out” and some airlines would close down and others would survive, resulting in a fitter, leaner and more customer-friendly industry.

Initially it appeared that this was indeed occurring. Small airlines like NEPC and bigger and stronger ones like ModiLuft and Air Deccan had to close or sell out. But, over time, for each airline that was shrinking or closing there appeared to be more than one emerging. And most were expanding their fleet and routes quite significantly. The irrationality of private decision-making under the market mechanism was more than visible.

Kingfisher was a relatively late entrant into the business with a business model the matched its promoter’s flamboyance. It would cater to the upper end of the market where the distinction between economy class and business class ended. And when Air Deccan ran into financial difficulties, promoter Mallya decided to acquire that company and combine his “luxury”, full-service airline (Kingfisher) with a no-frills twin, Kingfisher Red. All this was occurring at a time when the market was already showing signs of saturation, fuel prices were volatile, and cost consciousness was the prerequisite for survival. And decisions to expand that were not grounded on a viable business plan were a way of courting disaster. In the event, when rising fuel prices put pressure on costs, the Kingfisher myth was shown to be what it was: more a show than a business.

However, the problem with Kingfisher did not catch public attention for two reasons. First, it managed to fund much of the business with outside money, especially money in the form of credit from the banks. Second, it managed to reduce the cost of this capital by getting the banks to convert a part of this debt to equity. Interest on debt has to be paid even when a company makes losses. But dividends on equity need to be distributed only if profits are made.

These sources of support did not, however, save the business from losses that have created a gaping financial hole that needs to be filled. But here the airline and its promoter are exploiting the fact that it has grown rapidly to emerge as one of the larger carriers in the business in terms of market share. Like the American banks during the crisis, Kingfisher is being presented as “too big to fail”. The failure of the airline would lead to a sudden disruption of air traffic, it is said. It would result in a loss of access of finance to other airlines, which could trigger more bankruptcies in the business. It could badly damage the banks that are heavily exposed to the airline, which could have repercussions elsewhere in the economy. But most important for the government is that it would give liberalisation a bad name.

It is this which explains why both the Prime Minister, Manmohan Singh, and the Civil Aviation Minister, Vayalar Ravi, were quick to declare that Kingfisher needs to be “saved”. Though they have subsequently turned silent or retracted their statements, the effort to “bail-out” Kingfisher is on. The bailout strategy seems to be one in which the oil companies, the banks and the government (read the tax payer) would share the cost of rescuing the company suffering because of the wrong decisions of its original promoters.