The recent furore over the magnitude of frauds at public sector banks has added to the pile of non-performing assets the banking sector is saddled with. Big-ticket welfare programmes like the National Health Protection Scheme – dubbed Modicare – and the ambitious plan to double farmers' incomes by increasing the minimum support price to 1.5 times the cost of production were announced with much fanfare in the Budget speech. But if the system is not flush with funds for these schemes, the government has to go into debt; and that has a bearing on the economy.

Economists keep an eye out for the numbers coming out of the bond market. So do policy makers, mutual fund managers, and traders in equities and commodities. Government securities or bonds, may not directly affect one's personal finances, but the yield curve can be telling on the direction in which a country's economy is headed.

In November 2017, the international rating agency Moody’s upgraded India’s sovereign bond rating to Baa2 from Baa3 with a stable outlook. However, it also warned about high debt. Here is all you need to know about debt instruments and how they influence the economy.

What are bonds?

A bond is a debt instrument which acts as an IOU. It can be traded in financial markets like equities and other commodities. It is commonly used by governments to raise capital in order to fund domestic growth and development projects. Investors take on government debt, and in return, are assured a stream of revenue for the duration of the time it takes the bond to mature. Bonds issue coupons, which are interest payments made in part to the repayment of the capital that was borrowed. The final payment is made when the bond attains maturity. However, governments are not the only entities issuing bonds.

Who buys bonds and why?

Unlike equities, which are vulnerable to the vagaries of the stock market, investing in bonds is a relatively safer proposition since the capital is returned on maturity. The downside is that the returns on bonds may not be comparable to those of equities. Government bonds, also known as G-Sec, are issued by governments with maturity terms ranging from medium to long term.

Till recently, government bonds used to be bought and sold on the secondary market only by institutional investors like provident funds, mutual funds, insurance companies and banks. However, in 2017, the RBI changed the rules to allow retail investors, this is anybody with a PAN card, to buy government bonds in the primary market. The RBI is the institutional entity that has been mandated with selling sovereign debt securities, or government bonds.

[When investors buy securities directly from the entity that is issuing them, the transaction is said to have occurred in the primary market. The secondary market is where securities are traded after all the stocks or bonds issued by the issuing entity have been sold. The Bombay Stock Exchange is an example of a secondary market.]

Do only governments issue bonds?

Corporations also issue bonds to fund expansions and projects, or tide over budgetary deficits. Bonds issued by corporations are generally safer than equities, but some bonds offer an option to convert the instrument into stocks. Non-convertible corporate bonds offer coupons and function like any other bond.

How do bonds work?

Consider a bond that is issued by a company or government for Rs.100 with a coupon of 7% for a period of five years. This implies that every year, the issuer will pay interest of 7%, while the principal will be refunded after the bond matures. What drives the bond market is the fact that bondholders are free to sell their bonds before maturity.

The face value of a bond is what it sold for initially. Since they are transferable through sale in the bond market, their value fluctuates. The returns accrued by holders is measured by the yield, which is the rate of interest paid as coupons.

Yield is calculated as the coupon divided by the value of the bond. It is multiplied by 100 to be expressed in percentage. In effect, yield = (coupon/value)*100)

In the example considered above, if the face value of the bond fell to Rs.80, the yield would rise to 8.75%, that is (7/80)*100). Correspondingly, if the value rose to Rs.120, the yield would drop to 5.83%, that is (7/120)*100).

It should be noted that even if the value of a bond fluctuates, the amount that can be redeemed after the term of maturity is reached is the face value, which is Rs.100 in this case. Bond yield is inversely proportional to its current value. The greater the yield, the lower the current market price of the bond.

Bond yields as an economic indicator

Conventional metrics used by economists to diagnose the health of a country's economy include inflation, lending rate of the central bank, growth rate, and national income. However, bond yields are also a very prescient means of gauging the trajectory of an economy. As investors sell government bonds, prices drop, and yields increase. A higher yield indicates greater risk. If the yield offered by a bond is much higher than what it was when issued, there is a chance that the company or government that issued it is financially stressed and may not be able to repay the capital.

Enhanced risk with such bonds is offset by greater returns, adding to their appeal.

Government bonds are relatively more stable but low demand at auctions indicate low investor confidence in the country's economy. India's benchmark 10-year government bond has a yield of 7.39%, higher than that of Greece's 4.36%. The Greek government is currently rebuilding its economy after a sovereign debt crisis wiped out liquidity in the aftermath of the 2008 financial crisis. The long-term bond yields in the U.S. and the U.K. are 2.76% and 1.36%, while that of the Euro area 10-year government benchmark is 1.27%.

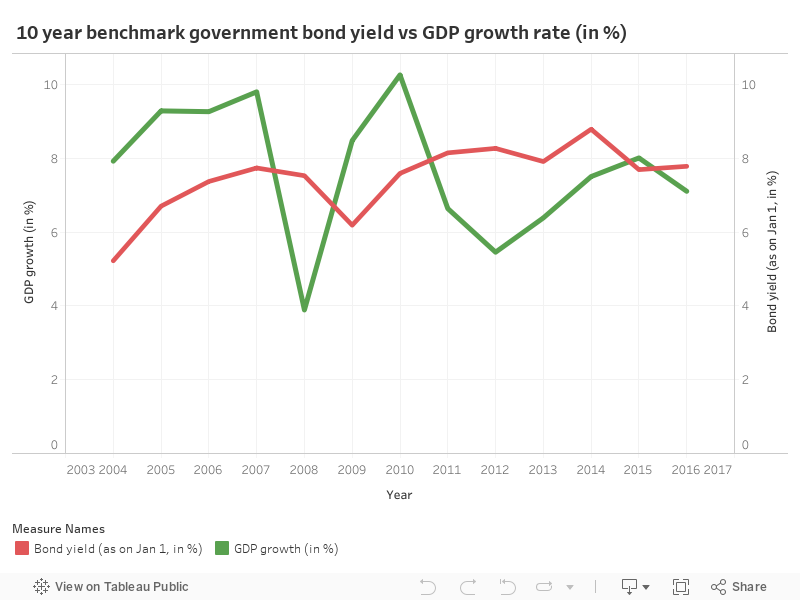

The Financial Times defines the yield on a risk-free government bond as being roughly "equal the rate of growth in the economy, plus the rate of inflation." In this case, the bond yields would mirror GDP growth, but the relationship between yields and economic activity is more complex especially in the case of developing countries like India. A whole host of factors including recessions, inflation, and bank rate set by central banks can have an impact on bond yields.

In developing countries like India where the government is among the biggest investors in the economy, bond yields can be a useful parameter in assessing economic health. It can be noted that at the height of the recession of 2008, the economy grew at only 3.89% while the yield on the benchmark 10-year government paper was 7.529%. This suggests that for FY2018, bond prices took a beating, but the government borrowed more in the form of bond issuance to tide over the slump in economic activity. However, the trend of loose correlation between economic growth and bond yield has held in the following years.

Unlike in countries where private enterprise drives the engine of growth, the trend of high bond yields is worrying in the case of India since it reflects on investor sentiment that is not entirely favourable to the prospect of the government taking on more debt.

How has the bond market reacted to the banking crisis?

The fiscal deficit is expected to widen even if the government issues new bonds to bankroll the populist schemes announced in the Budget. With banks sitting on a burgeoning pile of NPAs, the Reserve Bank of India (RBI) will have to raise liquidity in the market.

According to RBI norms, banks have to invest 19.5% of their total deposits in government bonds. This is called the statutory liquidity ratio (SLR). However, most banks invest over and above the requisite amount to be placed in government securities, or bonds. Bond yields have spiked over the past 18 months and consequently bond prices have dropped. Yield for the 10-year bond has gone up from 6.246% in November 2016 to 7.39% in March 2018.

Banks' bond portfolio falls into three brackets - held to maturity (HTM), available for sale (AFS) and held for trading (HFT). Under the RBI's statutory liquidity ratio regulation, banks have to hold 19.5% of their G-Secs to maturity. There is no restriction on the amount that can be held by banks for sale in the open market. Banks' HTF portfolios are not subject to mart-to-market (MTM) losses.

[MTM losses are said to have been incurred when an asset's value depreciates on paper even though no actual loss has taken place since it has not been sold.]

Despite recovering by about 25 basis points last week, the yield of India's benchmark long-term government bond remains higher than peers in developing economies. Government spending is expected to increase in the run-up to the general elections. Inflation, or expectations of inflation can drive up bond yields since any gains made by securities will be eroded by an increase in prices. The inflationary impact of certain newly announced schemes, like that relating to the farm sector, is still unknown. With greater government spending lined up this fiscal, the trajectory the yield curve will take up in the coming months could hold the key to predicting what the future holds in the run up to the general elections.