To the surprise of the UPA government, inflation just refuses to go away. Almost a year ago, when addressing a Chief Minister’s conference on food prices early in February 2010, Prime Minister Manmohan Singh declared: “The worst is over as far as food inflation is concerned. I am confident that we will soon be able to stabilise food prices.” Three months later, on more than one occasion, government spokespersons, like Chief Economic Advisor Kaushik Basu, declared that inflation had “peaked out” and was on a downward trend. Such statements are not surprising since in the current dispensation government representatives at the highest level are expected to talk down prices and talk up markets. It is not what you say but the confidence with which you say it that matters.

But there is reason to believe that the government did actually believe that prices would follow some sort of a cycle, and are more likely to rise slowly than at a rapid pace. One or two predictions of an impending decline are understandable. But, over the last year, almost every month or even week, one official spokesperson or the other (be it the Finance Minister, the Finance Secretary, the Deputy Chairman of the Planning Commission or the ubiquitous head of the PM’s Economic Advisory Council) declared that inflation is bound to moderate, in a voice tinged with surprise that it has not done so earlier.

This expectation came from a particular reading of the situation. Whenever prices did rise rapidly, it was attributed either to supply side factors such as a poor crop or to unavoidable factors like the “base effect”. Thus when the PM spoke in February last year he looked forward to a good monsoon and a better crop. And, if prices had been unusually low a year earlier, even a return to “normalcy” would reflect a high rate of inflation that must be discounted. Occasionally, of course, there was talk of hoarding and speculation, but only on the part of unscrupulous traders, who were exploiting temporary demand-supply imbalances.

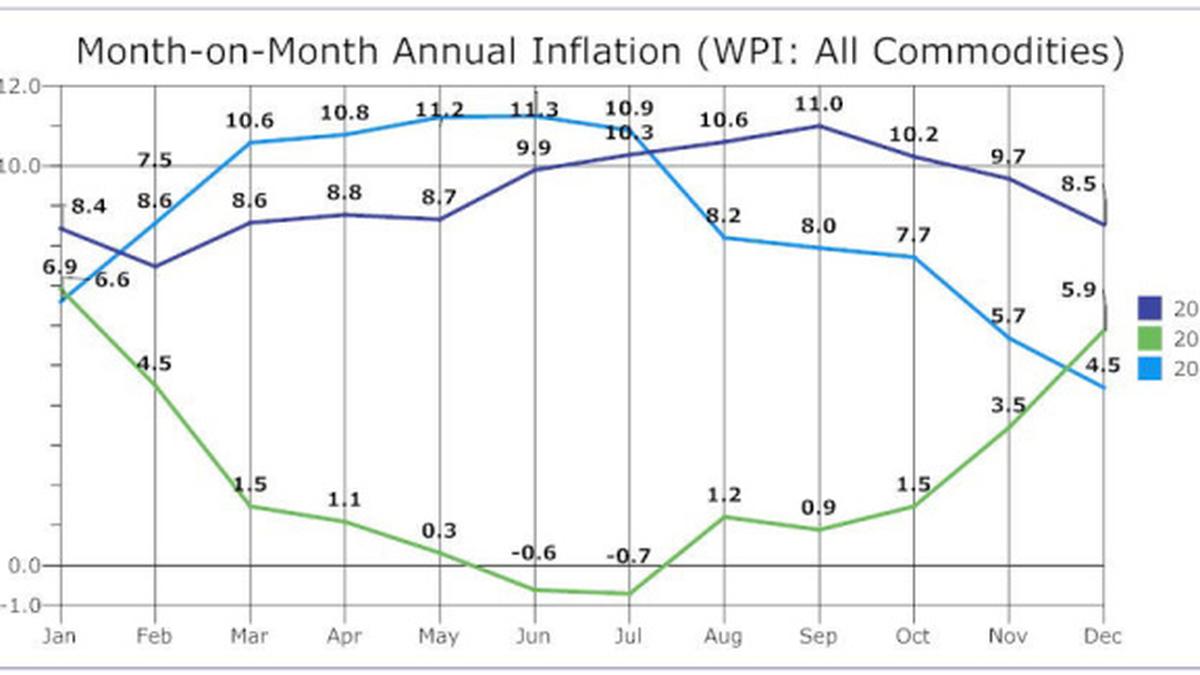

Experience has shown that these “beliefs” were patently false. Despite the fact that the monsoon has been much better in recent seasons, the month-on-month inflation rate as reflected even by the Wholesale Price Index, which stood at a disconcertingly high level in the first half of 2008, and then declined consistently between July 2008 and July 2009, accelerated subsequently and has remained at high levels throughout 2010. And weekly WPI movements are an indication this is likely to be true in January 2011 as well.

There are a number of features of this inflation scenario. The first is that, while it is not restricted to food alone, it has been substantially driven by food articles, which are more prone to speculative influences. Even when demand-supply imbalances are minor or absent, speculation can push up prices. The second is that within food articles, inflation has at different points in time affected different commodities, such as cereals, pulses, vegetables, eggs, meat and milk. Not all of these commodities are equally weather dependent and the prices of some are influenced by where administered prices are set. To attribute the trends in their prices solely to demand-supply imbalances or imported inflation is to avoid the conundrum. Third, when inflation does occur in some food items, be they onions, vegetables or even cereals, the rate of inflation tends to be extremely high, pointing to the role of speculation in driving prices in the short run. Finally, even when such influences are not at work there seem to be factors operative that keep the “all commodities” inflation rate high.

Even though it is still early to say, the trend over the last one-and-a-half years suggest that there are structural factors at work that are setting a higher floor to the inflation rate. They may be neutralised in the future. But even if they are, they could as well return to play a role subsequently. The government has recognised this structural, inflationary tendency in a peculiar, in fact patently absurd, way. It attributes the inflation to the demand-side effects of high growth. If people are richer because of an 8-9 per cent growth rate, they are bound to demand more. Since supply does not adjust, prices are bound to rise.

There are many assumptions here. That when GDP grows, those who need to buy and consume more cereals, pulses and vegetables garner a reasonable share of the benefits of that growth. Or that when GDP grows, the growth does not occur in large measure in the commodity producing sectors, or even if it does this happens only with a significant lag. That even though the “high growth” era began in 2004, it is only now that it has generated demand-supply imbalances. And, that if there is indeed a supply-demand imbalance the government is constrained, for whatever reason, to redress it by resorting to imports. Making such assumptions is not just wishful thinking, but avoiding the conundrum.

It is not that there are no demand-supply imbalances. India’s growth has indeed been lopsided. As has been argued by perceptive analysts, India’s high GDP growth was recorded in a period when the agricultural sector and a range of petty producers were experiencing a crisis, an aspect of which was the non-viability of crop production and therefore an extremely slow growth of agricultural output and GDP. At some point that long-term crisis, was likely to result in an unsustainable demand-supply imbalance.

But there are two other factors that are structurally embedded in the economic environment generated by the government’s neoliberal reform agenda adopted for two decades now. The first is a tendency where corporate consolidation in production and trade, decontrol that permits profiteering, a reduced role for public agencies and public sector firms and the withdrawal or curtailments of subsidies on a range of inputs, has pushed up costs and prices (including administered prices) substantially. As some have argued, India is increasingly a high input price and high output price economy, with a rising floor for many prices. The second is the role that speculation has to come to play, with liberalised trade, with the presence of large corporate players in the wholesale and retail trade and with the growing role of futures and derivatives trading in a host of commodities. Add the influence of these two factors to the underlying crisis in some commodity producing sectors and the long-term, structural inflation is more than partly explained.

The government of course does not consider these angles worth pursuing. The reason is partly ideological. It cannot bear questioning the outcome of reform. It cannot bear suggesting that corporate entry can lead to profiteering in a context of decontrol. It does not believe that speculation in futures markets can push up spot prices, and has banned some of these markets only because of public pressure. It cannot contemplate a larger role for the state and no role for corporate (domestic and foreign) players in the both wholesale and retail trade. In the event, all that the Prime Minister’s emergency meetings on the inflation issue could throw up is an inter-Ministerial group mandated to monitor short-term fire-fighting measures and promote actions that the government has claimed to be promoting for many years now.

What is more, in the midst of all this, on the basis of the liberalised pricing mechanism, the oil companies have been allowed to hike the prices of petrol a second time in quick succession. Given the role of public sector firms here, nobody would believe that a nod from the government was not obtained before the hike. If balance has to be maintained a diesel hike must follow. This government may go in for that as well. Doing this to the prices of what are universal intermediates in the midst of an inflation emergency might be seen by some as madness. If the belief that the people can be called upon to sacrifice real incomes because reform cannot be held back or reversed is a sign of madness, then possibly it is.