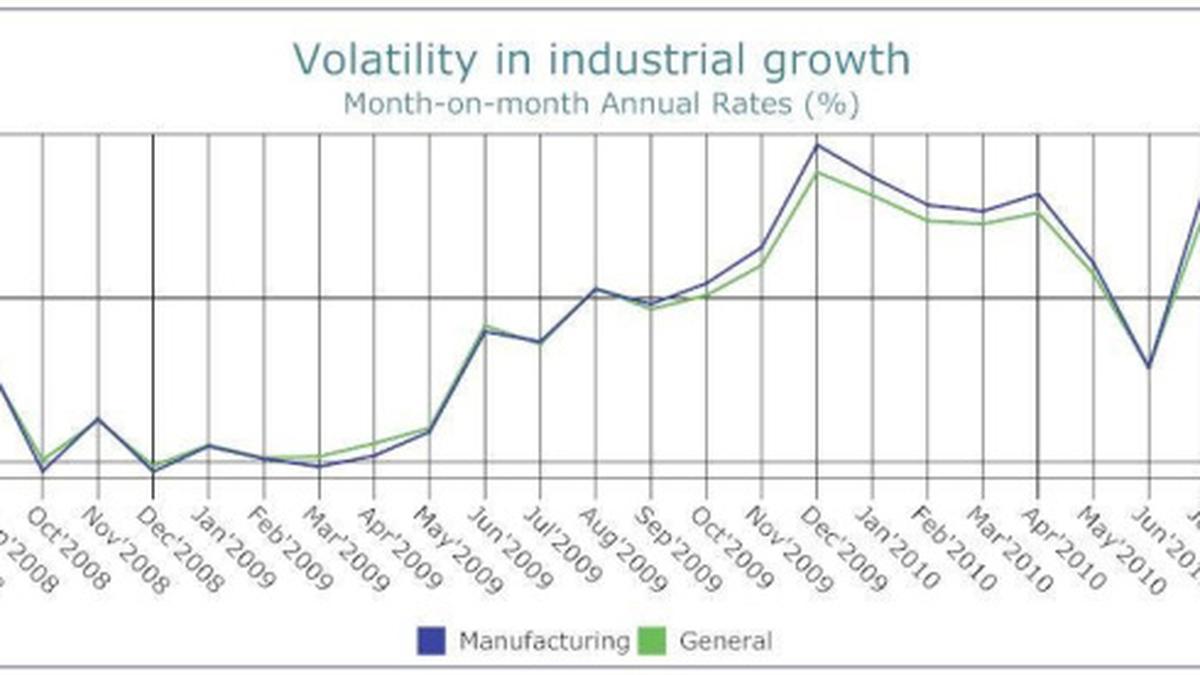

With the Indices of Industrial Production suggesting that the month-on-month annual growth rate of industry had fallen to a 15-month low of 5.6 per cent, industry sources and media pundits seem to have been overcome by a shadow of gloom. More so since the deceleration was led by the manufacturing sector that recorded a slowdown from 16.7 per cent in July to 5.9 per cent in August. Was this the first signal to suggest that the boom in India’s growth and the buoyancy of its stock markets is about to end, especially since the slowdown in industrial production has been led by a contraction in manufacturing production relative to August of the previous year? At least on the day on which the indices were released some investors seemed to answer yes, leading to a loss of momentum in the movement of the Sensex.

The fact of the matter is that the growth figures calculated using the provisional index for a single month say little. This comes through from the extreme volatility in the growth figures in recent times. Thus before falling to 5.6 per cent, the month-on-month growth rate of the IIP in July 2010 was a respectable 15.2 per cent. Moreover, if we examine the sector within manufacturing that has dragged down the index in August – namely capital goods – its 2.6 per cent decline comes after a 72 per cent rise in July 2010 relative to July 2009.

One reason month-on-month annual growth rates can be volatile is the base effect. A low industrial production in a particular month of the previous year implies that even “normal” production in the corresponding month of the subsequent year would deliver a high growth rate. But volatility of the kind we are seeing recently in the IIP cannot be explained by the base effect alone. There are clearly other factors at work. And these factors cannot be real economic trends, since investment cannot fluctuate to such an extent between two consecutive months that we get a 2.6 per cent decline in capital goods production in August after a 72 per cent increase in July, unless it is the effect of, say, a natural calamity of huge proportions.

Such movements can only be “statistical”. For example, there could be “missing numbers” or a shortfall or delay in reporting for some product or products included in the capital goods index in either the base period or the current period. This is normally “adjusted” for through, for example, assuming that output remained the same as in the previous month. If this occurs in bunched fashion in either the base or current period, the impact on the growth rate may be substantial. It is known that with the decline in the extent of influence or control exerted by the government on individual factories or plants after liberalisation, statistical reporting by the industrial sector has become slack. Firms do not see themselves as being under statutory pressure to collate and convey information on a timely basis. This problem has been compounded by the reduced attention and investment by the government in the collection of information which has often even been privatised. In the circumstances, reporting shortfalls would have only increased and could result in rather odd movements in a lead indicator like the Sensex (or even quarterly estimates of national income).

Why then are we seeing a growing and intense media and industry interest in these quick release “lead indicators”. In the days when information was seen as crucial for “planning” purposes, “short term” numbers such as month-on-month growth rates would have been frowned upon and seen as misleading. It is in today’s liberalised world that they seem to have acquired a whole new status. One reason is that they are pounced upon by financial journalists in the print media and 24 hour news channels needing material to fill their column spaces and their excess air time. But there must be a reason why the system needs these media sources as well.

The answer seems to lie in the undue importance financial markets have acquired and the role of speculative operators in those markets. Information overload is a boon to the speculator since it offers “explanations” for what are in fact engineered shifts in the markets. It also provides material needed to manipulate markets. Thus, immediately after the August figures were released the stock market appeared to be reacting with panic, ostensibly on the grounds that the IIP figures were signalling that the growth and profits that warranted the high price-earnings ratios the market reflected were coming to an end. Neither was the earlier expectation of such growth warranted nor was the sudden change in sentiment. Players who mattered clearly did not believe all this. Not surprisingly a day later the Sensex soared by 484 points, this time for a wholly different “reason”. The sharp rise was now attributed to expectations that worsening employment figures in the US would result in another round of “quantitative easing” or the infusion of cheap liquidity by the Federal Reserve, some of which would find its way to the Indian market. There always is some information to “explain” a market trend. This puts value even on information that would otherwise be suspect.

There are also other ways in which any information can be put to self-serving uses. Thus, pouncing on the “news” that the month-on-month IIP growth had fallen to a 15-month low, the Secretary General of FICCI reportedly declared: “There are number of worrying signals in the August IIP data. Negative growth in key sectors such as capital goods, apparels, consumer non-durables and chemicals is a cause for concern and with further appreciation in the rupee and hardening of interest rates, the growth of the manufacturing sector may be significantly affected. We would urge the Government to intervene and address the issue of rupee appreciation to further arrest the slowdown in export intensive sectors like apparels. Also, any further hike in interest rates could impact consumer durables and the automotive sector.” Clearly bad news can be put to good use.