Sporadic news on the recent behaviour of foreign institutional investors (FIIs) has strengthened the impression that there has been a flight of capital out of India. Many, including government spokespersons, attribute the rupee’s decline and subsequent weakness to the withdrawal of capital from the country. India could have managed its balance of payments deficit, it is argued, if international developments such as a possible tapering of the Federal Reserve’s policy of quantitative easing had not resulted in a retreat of foreign investors.

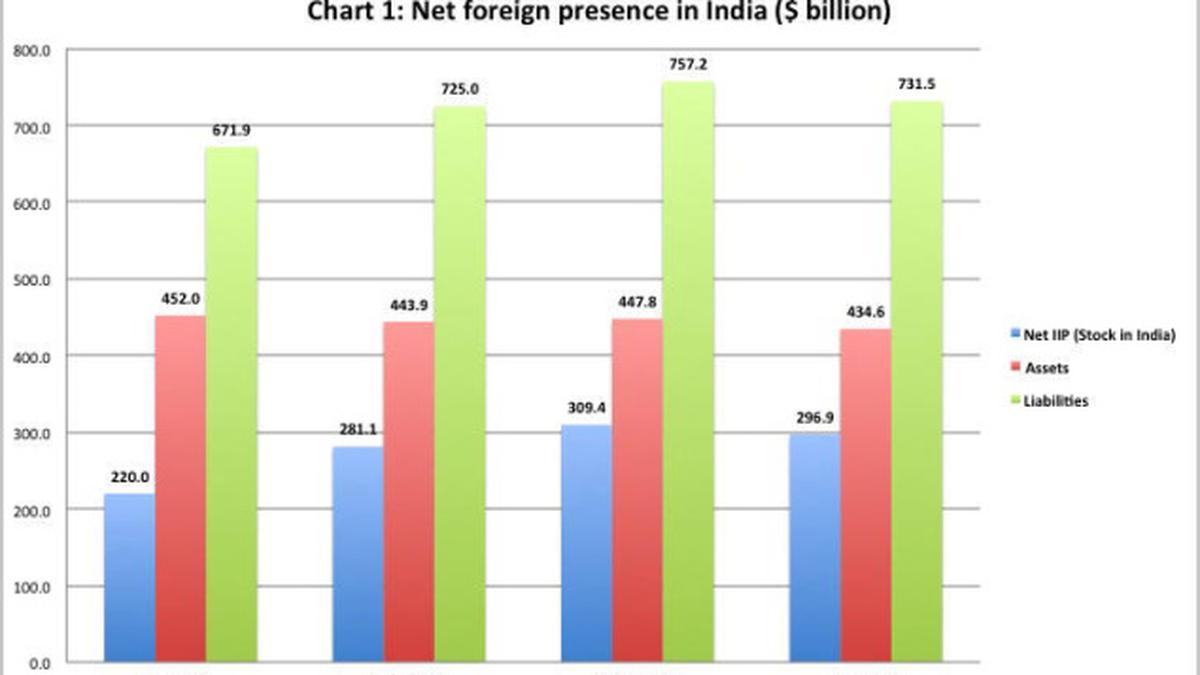

With the release of data on changes in India’s Net International Investment Position for the April to June 2013 period it is possible to assess the weight of this argument. The April to June quarter was the period when the rupee depreciated from its level of close to Rs.54-to-the-dollar to Rs. 60-to-the-dollar, with almost the entire decline occurring over May and June. The evidence suggests (Chart 1) that India’s net investment position, or the net claims of non-residents on India, measured as the excess of non-resident capital that had accumulated in the country over total assets held by Indian residents abroad, had declined during these months by $12.5 billion, with the country’s assets abroad having fallen by $13.2 relative to the previous quarter while foreign assets in India fell by a larger $25.7 billion.

These aggregate numbers reflect three tendencies. First that the situation during April-June 2013 was completely different from that in the immediately preceding quarters, when both asset accumulation abroad by residents and asset accumulation within the country by non-residents were rising. Second, that more capital had exited from India during this quarter than had been repatriated back to the country, requiring an examination of the categories of capital flow that were responsible for these inter-temporal changes in the inflows and outflows of capital. And, finally, that investors were indeed ‘fleeing’ from India in this period when the rupee was in decline.

A noteworthy feature of the recently released numbers (Chart 2) is that foreign investments categorised in the official statistics both as ‘direct investment’ and as ‘portfolio investment’ declined — the former by $13.8 billion (5.9 per cent) and the latter by $13.7 billion (7.4 per cent). In principle, direct investment is treated as being that by investors with a long term interest in dividend returns from the country and portfolio investment as that by investors with short term horizons and interest in capital gains. This is expected to make the former more stable and latter more volatile. The evidence suggests that this is not a distinction the categorisation actually makes. Even investment categorised as ‘direct’ includes a component that displays volatility.

Were the uncertain economic conditions resulting in the exit of capital from India also responsible for the decline in investment abroad by residents? This does not seem to be case (Chart 3) since the decline in assets held abroad by resident agents was not the result of a fall in foreign direct investment by them but because of a decline in the foreign reserves held by the central bank. On the other hand, resident investment abroad remained stable. That is India’s asset holding abroad fell because the Reserve Bank of India was using a part of its reserves to stabilise a weakening rupee, even if unsuccessfully. Reserve assets fell by $9.6 billion during April-June 2013 compared with the immediately preceding quarter.

This has implications for the factors responsible for changes in India’s international investment position. It could be argued that foreign investors were pulling investment out of India because of external developments, such as the possibility that the Federal Reserve’s policy of ‘quantitative easing’ would be ‘tapered’ down, with a reduction in the access of investors to cheap money. But, even to the extent that this was true, the impact of that on the Indian rupee would depend on how important such investments were for financing India balance of payments. Given India’s large current account deficit, or excess of foreign exchange expenditures over foreign exchange earnings, those flows were indeed important. As net flows turned negative, the current account deficit emerged an important and more fundamental explanation of the rupee’s weakness. And it is that weakness that partly triggers the fall in the reserve assets held by the central bank.

A large current account deficit and a weakening rupee also adversely affect investor sentiment, which (besides ‘external’ factors) contributes in turn to a decline in foreign investment in the country. So while capital flight from India does matter when explaining the rupee’s position and the uncertain economic environment, the country’s balance of payments position is the more fundamental weakness that can and needs to be addressed.