The IMF has recently declared that emerging markets that are currently experiencing a capital inflow surge have reason to impose controls on cross-border capital flows. This is a significant shift in IMF policy given its earlier predilection to strongly recommend an opening of the capital account in developing countries. It has been necessitated by evidence of the dangers associated with excessive cross-border flows. As yet informal guidelines issued by the IMF state that short-term capital controls are “squarely within the toolkit” for managing these hot money flows. In making this recommendation it is merely endorsing the actions already taken by countries such as Brazil.

Surprisingly, the Indian government is currently pushing to further liberalise rules governing the inflow of foreign capital. In recent months, Indian government spokespersons have been expressing concern that the inflow of foreign direct investment into the country has slowed down considerably. This has been offered as justification for further liberalisation of rules and regulations governing such flows.

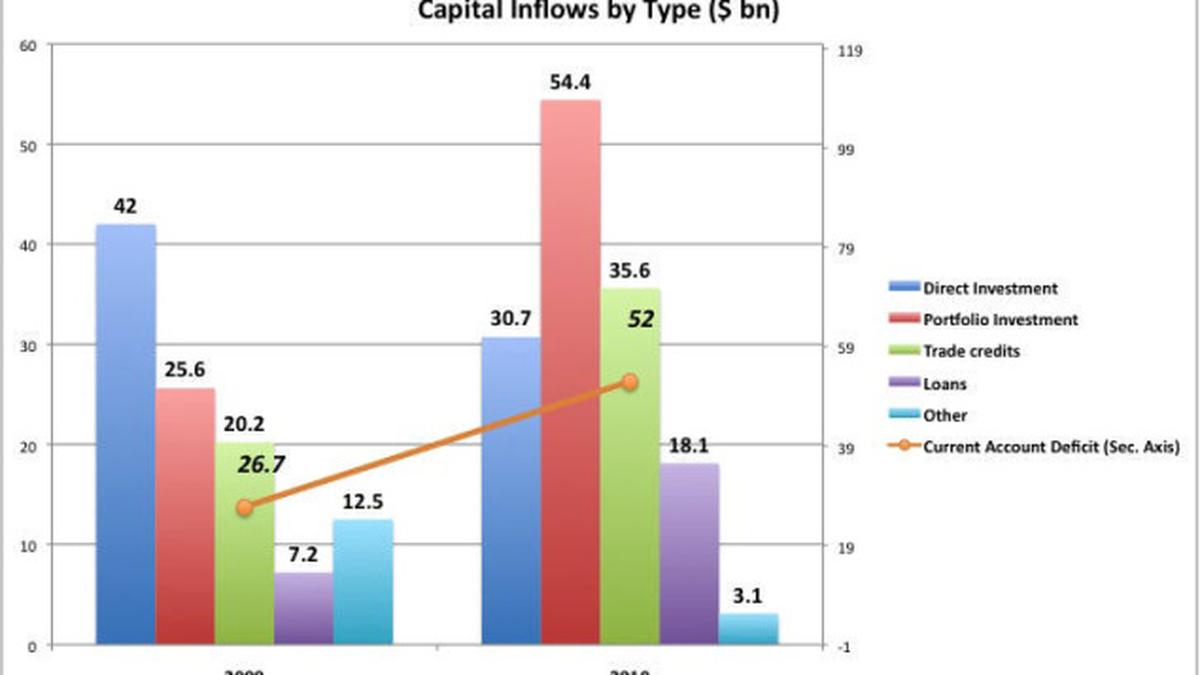

On the surface, figures on India’s net international investment position do seem support the official assessment. While (gross) portfolio flows more than doubled from $25.6 billion in 2009 to $54.4 billion in 2010, direct investment fell from $42 billion to $30.7 billion. However, over both calendar years (2009 and 2010) during which the recovery from the global financial crisis has been underway, both direct and portfolio flows into the country have been significantly large.

Thus, while the data may point to recent slowing of direct investment flows, the overall picture is one of substantial inflows after the crisis. What is more, the combined value of trade credits and longer-term loans, incurred largely by the Indian private sector, has also risen by more than $25 billion between 2009 and 2010. As a result, India’s gross financial liabilities increased by $87.9 billion in 2009 and a huge $120.7 billion in 2010.

It needs to be noted that these capital inflows into the country are not driven by its current account financing requirements. In fact, as the accompanying Chart shows, the current account deficit was almost covered by the volume of portfolio flows alone. In the event, India was accumulating large international financial liabilities for reasons other than the financing of its net current account requirements.

The explanation for the high levels of capital inflows is now well known. With governments and central banks in the developed countries infusing huge volumes of cheap capital into their economies in their efforts to address the financial crisis and the possible insolvency of their financial firms, the world has been awash with liquidity. In response, financial firms have acquired capital at near zero interest rates and invested it wherever returns were positive, and especially where they are significantly so. This has delivered quick profits and helped restore the profitability of the financial sector, even while the real economy in the developed countries has languished. Emerging markets such as India, which were less affected by the financial crisis, were lucrative destinations for this kind of “carry trade”, involving borrowing in one currency at a low interest rate and investing in another at a much higher rate. Not surprisingly they have experienced a capital inflow surge in the aftermath of the crisis.

The implication of this is that a significant share of recent capital inflows into emerging markets is reflective of the speculative thrust of global financial firms rather than the flow of productive capital to the less developed regions of the world. This makes them problematic for three reasons. First, they are flows that do not have any long-term interest, and can exit as and when conditions elsewhere in the world warrant a change in the decisions of financial speculators. This feature of capital inflows is missed in the now meaningless distinction between “direct” and “portfolio” investment in the statistics.

Conceptually that distinction is meant to reflect the difference between capital with a long term productive interest in the host economy, looking for returns in the form of profits repatriated as dividends, and short term speculative capital, looking for returns in the form of gains from capital appreciation. In practice, the distinction is based on an arbitrary share of equity in the target firm held by the investor. Normally, a foreign investor holding 10 per cent or more equity in a single firm is treated as a direct investor and the investment a direct investment, independent of the nature of the investor concerned and the intentions of that investor.

As the size of finance capital has increased, a host of firms varying from investment banks to hedge funds and private equity firms have tended to acquire 10 per cent or more equity in a single emerging market target for purely speculative purposes. Privileging them as “direct” investors, as opposed to portfolio investors, is without any real basis.

The second difficulty with the recent surge in capital flows is that it results in the quick accumulation of foreign liabilities that imply substantial future commitments in foreign exchange terms. Those commitments involve not just the possible repatriation of the original investment, but also the repatriation of whatever returns such investments may earn in the domestic economy. To the extent that the inflows do not substantially strengthen the productive base of the host economy, especially the productive base in the tradables sector that could help earn foreign exchange through exports, the accumulation of such liabilities implies a draft on the future foreign exchange earnings of the rest of the economy. Since such earnings are not certain, this implies an increase in external vulnerability.

Finally, the surge in capital flows imparts upward pressure on the currency of the host economy, threatening appreciation that could undermine its export competitiveness. This forces the central bank in the host country to buy up foreign exchange and accumulate reserves in order to stabilise the currency.

Besides the fact that this creates problems for monetary management, it also implies a national loss suffered in foreign exchange, since the returns earned by the investors in the host economy are normally many multiples of the returns earned by the central banks from the liquid assets in which reserves are invested.

For these and other reasons the recent capital inflow surge that increases India’s international financial liabilities is a cause for concern and requires capital controls. It is strange therefore that the government is using the groundless distinction between direct and portfolio investment and the resulting short run change in the composition (and not magnitude) of foreign capital inflows to liberalise capital inflows into the country. This is perhaps one occasion when it should listen to the IMF.