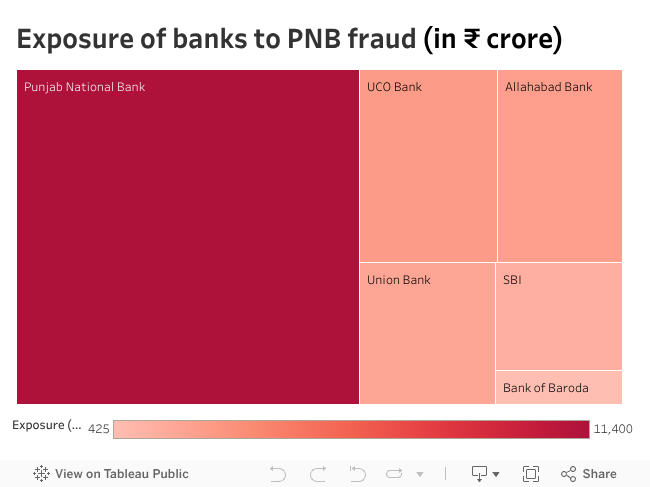

Bad loans have long been the albatross around the neck of India's banking sector, and the detection of fraudulent transactions totaling Rs.11,400 crore at Punjab National Bank's (PNB) Brady House branch in Mumbai, has only served to highlight the import of the situation. The scam, which involves diamantaire Nirav Modi's eponymous range of jewelry stores, accounts for nearly a quarter of PNB's consolidated net worth of Rs.43,164 crores, as filed by the bank, for the year ended March 2017.

The government has swung into action, with multiple agencies currently probing the modus operandi behind the biggest financial fraud in recent years. It was found that funds were siphoned off from the bank by employees who willfully manipulated SWIFT, the electronic messaging system used for overseas funds transfer. This was accomplished by issuing letters of understanding (LoU) on behalf of companies associated with Nirav Modi, to avail credit from overseas branches of Indian banks.

None of the aforementioned fraudulent transactions were registered on the bank's Core Banking Solution (CBS), thus enabling it to go unnoticed. LoUs were advanced in favour of Nirav Modi's firms to overseas branches of Indian banks, for the import of pearls for a period of one year. The Reserve Bank of India (RBI) mandates that the maximum time frame for such a transaction is 90 days from the time of shipment.

Allahabad Bank, Union Bank, Axis Bank, among others offered credit based on the LoUs issued by PNB, adding to their exposure to the scam. Ironically, the Nirav Modi scam has gypped PNB of more than twice the Rs.5,473 crore cash infusion it received under the government's bank recapitalisation plan.

Here is all you need to know about how banks disburse credit to businesse engaging overseas trade.

What is an LoU?

A letter of undertaking is a document issued by a bank, guaranteeing the credit-worthiness of a client for overseas export payments. The bank stands as guarantor for the client and is liable for the repayment of the principal and interest of the amount for which the LoU was drawn. Four entities has signatories to a LoU - the issuing bank, the receiving bank, the beneficiary and the exporter. In the Nirav Modi case, LoUs were issued by bank employees who colluded with the accused and misused their access to PNB's SWIFT account for the same. A loophole in the bank's internal transaction messaging system, the CBS, was exploited to avoid detection.

What is SWIFT?

SWIFT is the acronym for the Society for Worldwide Interbank Financial Telecommunications. It forms the backbone of ecosystem used by banks for cross-border money transfer. SWIFT is a messaging network used by lenders for inter-bank money transfer involving overseas transactions. Standard encryption is applicable to messages sent via SWIFT to ensure its safety. However, the system is not infallible, and is vulnerable to hacking by extraneous agents, as was the case in the heist of $81 million from Bangladesh’s central bank, and also as bank insiders, who can manipulate the system at the bidding of rogue clients.

SWIFT was formed in 1973 by a group of seven banks. The Brussels based member-owned cooperative has since gained near-universal acceptance, with over 11,000 financial institutions from 200 countries enrolled on its network. Its precursor, Telex, which operated on a public switched network of teleprinters, was rendered defunct since it was prone to the error of operators, and was relatively unsafe for the transmission of sensitive financial information.

The SWIFT cooperative is controlled by around 3,500 financial institutions which act as the shareholders, who in turn elect a Board of 25 Independent Directors. The highest decision making body of the SWIFT is representative of all the major financial institutions of the world. Its functioning is overseen by the central banks of the G-10 countries, and the European Central Bank.

How does SWIFT work?

The messaging network is a code-based product which uses unique identification codes to link all the stakeholders in an overseas financial transaction. The key components of the package are the Business Identifier Code (BIC), the International Bank Account Number (IBAN), and the Legal Entity Identifier (LEI).

The BIC is used for identifying parties to a transaction and routing the business through established channels. BIC is the International ISO standard ISO 9362:2014.

In effect, the code can vary between eight and 11 characters. The first four characters (alphanumeric) denote the name of the issuing financial institute. The next two characters stand for the country code, while the last of the two mandatory characters indicate the location, or city code. The issuing financial institution can optionally postfix three characters to denote individual bank branches.

If a client wants to transfer money from his home branch to another bank situated overseas, the bank account details and the SWIFT code of the recipient's bank are required to initiate the transaction.

Likewise, a SWIFT code is necessary to raise credit from international bank accounts. This was the case in the fraud at PNB's Brady House branch, where employees of the bank shared the institution's SWIFT password with individuals representing firms owned by Nirav Modi, thereby resulting in the issuance of duplicitous LoUs via SWIFT.

What is CBS?

Core Banking Solution is a software product that links all the customers of a bank, regardless of their home branch. The CBS' primary objective is to centralise details of financial transactions, and maintain a universal database of the credit-history of customers of individual branches.

What went wrong in the Nirav Modi case?

According to a report filed by the CBI, Reuters reported that the branch deputy manager at Brady House, Gokulnath Shetty, issued a series of fraudulent LoUs to overseas branches of Indian banks to provide credit to a group of jewelry companies associated with Nirav Modi. Mr.Shetty, who was privy to the SWIFT password of the bank, sent messages on the network, with the connivance of a junior colleague.

The loophole in the software framework of the bank was the patchy implementation of its CBS and its non-linkage with SWIFT. Since both the systems were not integrated, employees were required to manually log SWIFT activity. This rendered transactions vulnerable to the wiles of rogue employees, who could choose not to log transactions, and unilaterally fudge records. A CBI official told Reuters on the condition of anonymity, that 150 fraudulent LoUs were issued during a seven year period.

How many banks have exposure to the scam?

The scam has set PNB - India's second largest public sector bank - back by Rs.11,400 crore. Other banks which gave credit to Nirav Modi's based on LoUs issued by PNB have also been exposed to the scam. The highest exposure is to UCO Bank, which has been defrauded of Rs.2,635. Allahabad Bank and Union Bank have also seen the erosion of their assets to the tune of Rs.2,400 crore and Rs.1,920 crore respectively.

Do the overseas branches of Indian banks make a profit on import credit?

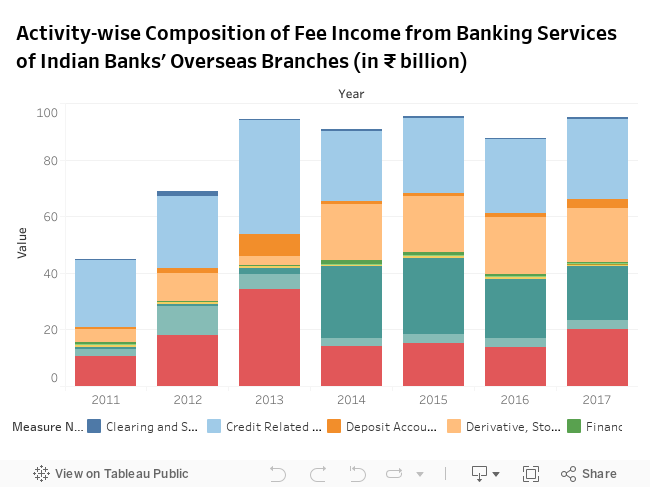

The RBI's Survey on International Trade in Banking Services for the years 2010-17 reveals that branches of Indian banks operating abroad have made profits on auxiliary services rendered by the bank "based on explicit/implicit fee/commission charged to customers."

The total credit extended by Indian banks abroad amounted to Rs.8,661.3 billion in 2016-17, on which it made an income of Rs.436.1 billion. Interest income accounted for Rs.381.3 billion of the gross income.

Indirect accrual of profit through the extension of financial services has plateaued after 2013. The total income from auxiliary services amounted to Rs.94 billion in 2017, of which credit related services, trade in derivatives, equities comprised Rs.28.3 billion and Rs.19.2 billion respectively.

Which countries are most lucrative for overseas banking services?

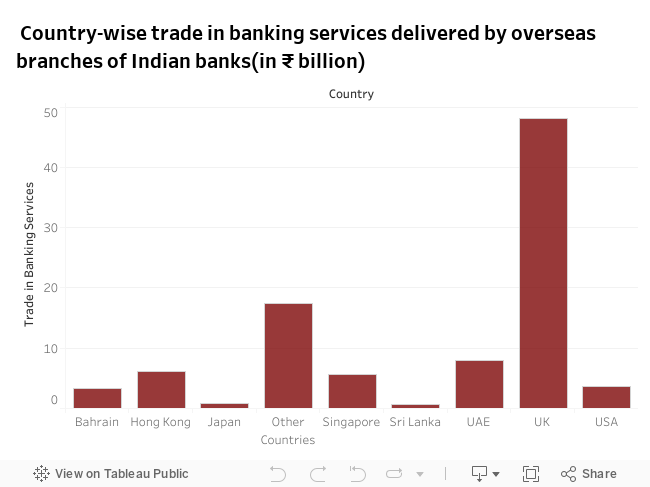

The RBI's Survey on International Trade in Banking Services: 2016-17 reveals that more than half of the Rs.94 crore accrued by overseas branches of Indian banks, originated in the United Kingdom. Of this, Derivative, Stock, Securities, Foreign Exchange Trading services, and Credit Related Services accounted for Rs.15.9 billion and Rs.13.9 billion respectively.

Branches of Indian banks in the United Arab Emirates (UAE), Singapore, and Hong Kong totaled Rs.8 billion, Rs.5.7, and Rs.6.2 crore.

However, the magnitude of the scam involving PNB underlines the fact that all is not well with the country's banking system, and public sector banks, in particular. The whereabouts of Nirav Modi - the man at the centre of the biggest white collar crime in India since the $1.47 billion Satyam scam - remain unknown.